Recently the whole "if your p(doom) is high, you should short the market" thing has been going around. Let's say the market prices in a 0.1% chance of extinction per century, and you think there's a 50% chance we're dead in the next 25 years. This is about 12 bits of evidence.

- How much profit is it even reasonable to expect someone to make from 1 bit of evidence?

- Is this a constant function of the bits which is calculable like e.g. a Kelly bet? Or does it depend on the market?

- If the latter, does it ever make sense to short things at all based on p(doom)? I assume not, since shorting is generally stupid high-risk for an uninitiated trader (as I understand it).

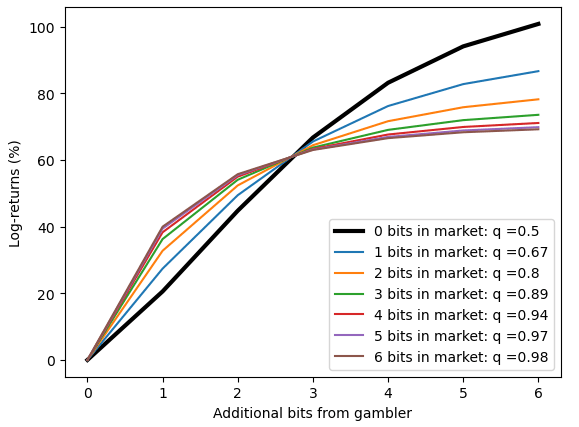

Consider: everyone else thinks a company share has a 0.1% chance of being worth $10 tomorrow and a 99.9% chance of being worth $0. I think the chance is 50:50. Therefore the stock price is $0.01 today. If I have $100 in the bank, I maximize expected log(money) by spending fully half of my money on it. By my reckoning the maximum log-expected money is $1581, which corresponds to about a 16-fold increase over $100. Which is not 10 bits of alpha!

PS not looking for investment advice here, just looking for maths.

This is similar to the answer I got from

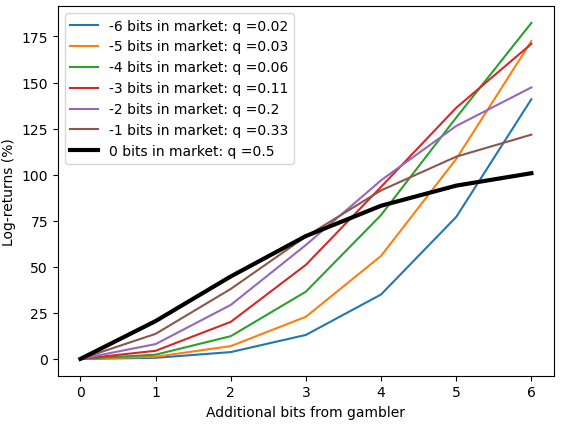

o1-previewin ChatGPT when I originally asked with OP's post as the text, so that's pleasant to see. (I didn't post anything here because I was unsure and wasn't checking it in enough detail to repost, and so didn't believe in publishing it without being able to improve it.)I thought there might be some relationship at first with an appropriate transformation, but when I recalled how Kelly requires both edge and net worth, and the problem of frequency of payoffs, I lost my confidence that there would be any simple elegant relationship beyond a simple 'more information = more returns'. Why indeed would you expect 1 bit of information to be equally valuable for maximizing expected log growth in eg. both a 50:50 shot and a 1,000,000,000:1 shot? Or for a billionaire vs a bankrupt? (Another way to think of it: suppose you have 1 bit of information on both over the market and you earn the same amount. How many trades would it take before your more informed trade ever made a difference? In the first case, you quickly start earning a return and can compound that immediately; in the second case, you might live a hundred lives without ever once seeing a payoff.)