Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period. - Wikipedia, GDP

Due to inflation, GDP increases and does not actually reflect the true growth in an economy. That is why the GDP must be divided by the inflation rate (raised to the power of units of time in which the rate is measured) to get the growth of the real GDP. - Wikipedia, Real GDP

The two quotes above reflect how I used to think about real GDP growth: it’s roughly the growth in economic production (as measured by dollar worth of outputs), discounted for inflation. This picture turns out to be extremely misleading, especially when using GDP as a growth measure. Forget complaints about how GDP doesn’t measure happiness, or leisure time, or household work, or “the health of our children, the quality of their education or the joy of their play”. Even if we accept the dollar value of goods as a proxy for whatever purpose we have in mind, GDP (as we actually calculate it) is still a wildly misleading measure of growth. In particular, it effectively ignores major technological breakthroughs.

A Puzzle

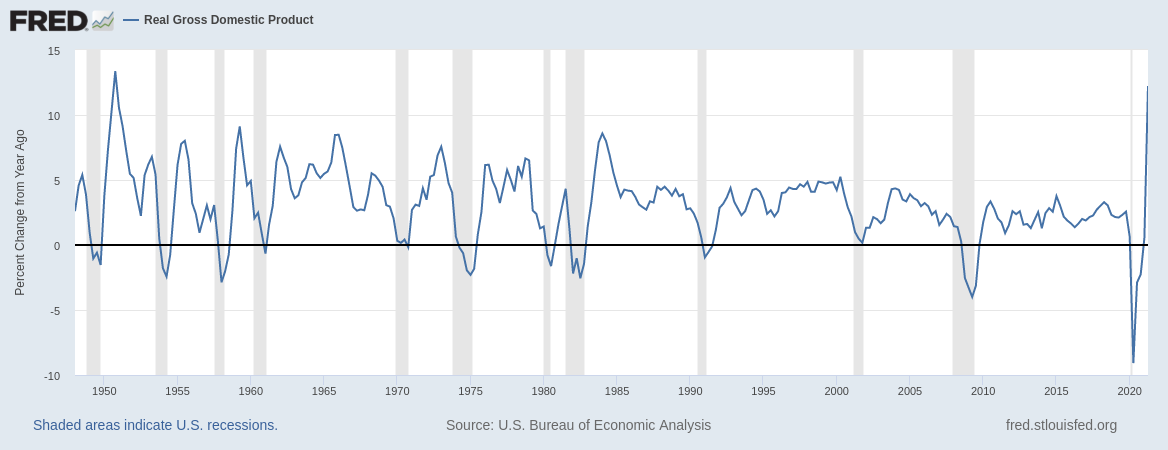

Here’s real GDP of the US for the last ~70 years, from FRED:

According to this graph, real GDP has grown by roughly a factor of 6 since 1960. That seems… way too low, intuitively. Consider:

- I’m typing this post on my laptop (which conveniently has a backspace button and everything I type is backed up halfway around the world and I can even insert images trivially)...

- while listening to spotify…

- through my noise-canceling earbuds…

- and there’s a smartphone on my desk which can give me detailed road maps and directions anywhere in the US and even most of the world, plus make phone calls…

- and oh-by-the-way I have an internet connection.

I’d expect the equivalent of any one of these things in 1960 would have cost at least a hundred times the annual income of an average person if it was even possible at all. Just from these five things alone, it seems like real GDP ought to have grown by a factor of hundreds.

… and yet, whatever formula we’re using for real GDP says it's only grown by a factor of 6. What gives? How the heck is real GDP computed that makes it so low? What exactly is it measuring?

Real GDP Is Not Nominal GDP Divided By Inflation

First things first: real GDP is not calculated by dividing nominal GDP by inflation. It’s calculated largely separately from nominal GDP; the textbook approach is to add up the total dollar value of goods (just like for nominal) but at prices from a fixed year. That way, we only count changes in total output resulting from changes in the amounts of goods produced.

An example: we have an economy with two goods, apples and brass. In year 0, 1 unit of apples costs $1, 1 unit of brass costs $1, and people produce/consume 3 units each of brass and apples. In year 1, an amazing new technique is discovered for brass-production. Brass prices fall by a factor of 10, and people produce/consume five times more brass (15 units). Meanwhile, both price and production/consumption of apples stays roughly the same.

| Apple Price | Apple Quantity | Brass Price | Brass Quantity | |

| Year 0 | $1/unit | 3 units | $1/unit | 3 units |

| Year 1 | $1/unit | 3 units | $0.1/unit | 15 units |

Calculations:

- GDP in year 0 (at year 0 prices): (3 apple-units)*($1/apple-unit) + (3 brass-units)*($1/brass-unit) = $6

- GDP in year 1 (at year 0 prices): (3 apple-units)*($1/apple-unit) + (15 brass-units)*($1/brass-unit) = $18

- GDP growth: $18/$6 = 3

This seems pretty reasonable. Indeed, in our puzzle about GDP growth since 1960, I said:

I’d expect the equivalent of any one of these things in 1960 would have cost at least a hundred times the annual income of an average person if it was even possible at all. Just from these five things alone, it seems like real GDP ought to have grown by a factor of hundreds.

That intuition is implicitly a calculation of real GDP at 1960 prices: I’m saying that at 1960 prices, the electronics on my desk would cost a fortune. If everybody now has goods which would cost hundreds of times the typical annual income in 1960, then that implies that real GDP in 1960 prices has grown by at least a factor of hundreds.

… but clearly that’s not how the economists at the BEA actually compute real GDP, since they only calculate a factor-of-6 increase since 1960. So what’s different?

Real GDP Is Calculated At Recent Prices

Real GDP isn’t calculated using prices from 1960 (or 1900, or some other time long ago). It’s calculated using recent prices. Wikipedia again:

… the UNCTAD uses 2005 Constant prices and exchange rates while the FRED uses 2009 constant prices and exchange rates, and recently the World Bank switched from 2005 to 2010 constant prices and exchange rates.

… wait, they switch which year’s prices are used?

Ok, before we get into baseline prices moving, let’s go back to our apples-and-brass example and see what happens if we use “recent” prices (i.e. year-1 prices) rather than “old” prices (i.e. year-0). Here’s the table again:

| Apple Price | Apple Quantity | Brass Price | Brass Quantity | |

| Year 0 | $1/unit | 3 units | $1/unit | 3 units |

| Year 1 | $1/unit | 3 units | $0.1/unit | 15 units |

Calculations:

- Real GDP in year 0 (at year 1 prices): (3 apple-units)*($1/apple-unit) + (3 brass-units)*($0.1/brass-unit) = $3.3

- Real GDP in year 1 (at year 1 prices): (3 apple-units)*($1/apple-unit) + (15 brass-units)*($0.1/brass-unit) = $4.5

- Real GDP growth: $4.5/$3.3 = 1.36

… so rather than factor-of-3 growth (i.e. 200% growth), we see factor-of-1.36 (i.e. 36%). What’s going on here?

The key is the drop in price of brass. In year-1 prices, brass costs next-to-nothing. So, when we calculate in year-1 prices, brass has very little weight in real GDP; even a very large increase in brass production contributes a relatively small bump to real GDP. The more brass prices fall, the less brass will contribute to real GDP growth (as calculated in year-1 prices).

More generally: when the price of a good falls a lot, that good is downweighted (proportional to its price drop) in real GDP calculations at end-of-period prices.

… and the way we calculate real GDP in practice is to use prices from a relatively recent year. We even move the reference year forward from time to time, so that it’s always near the end of the period when looking at long-term growth.

Real GDP Mainly Measures The Goods Which Are Revolutionized Least

Now let’s go back to our puzzle about growth since 1960, and electronics in particular.

The cost of a transistor has dropped by a stupidly huge amount since 1960 - I don’t have the data on hand, but let’s be conservative and call it a factor of 10^12 (i.e. a trillion). If we measure in 1960 prices, the transistors on a single modern chip would be worth billions. But instead we measure using recent prices, so the transistors on a single modern chip are worth… about as much as a single modern chip currently costs. And all the world’s transistors in 1960 were worth basically-zero.

1960 real GDP (and 1970 real GDP, and 1980 real GDP, etc) calculated at recent prices is dominated by the things which are expensive today - like real estate, for instance. Things which are cheap today are ignored in hindsight, even if they were a very big deal at the time.

In other words: real GDP growth mostly tracks production of goods which aren’t revolutionized. Goods whose prices drop dramatically are downweighted to near-zero, in hindsight.

When we see slow, mostly-steady real GDP growth curves, that mostly tells us about the slow and steady increase in production of things which haven’t been revolutionized. It tells us approximately-nothing about the huge revolutions in e.g. electronics.

(Disclaimer: Real GDP Is Sometimes Computed Differently)

One word of caution, before we get to the main takeaways: real GDP at fixed (recent-year) prices is not the method used by everyone for every number called “real GDP”. In fact, the real GDP graph at the beginning of this post uses a different method - the BEA (which calculates the “official” US GDP and produced the numbers in that graph) switched from fixed prices to “chaining” in 1996. Appendix 1 of the NIPA Guide has useful details if you’re interested, and these slides give some of the reasoning. The new method is generally messier and less intuitive, but tries to correct for some of the shortcomings of fixed prices.

I played around with it a bit, and I think the qualitative takeaway is basically similar for purposes of thinking about long-term growth and technological progress (e.g. something like Moore’s law). Also, it sounds like fixed prices are still the standard thing in most places, although I haven’t looked into how other sources (like the World Bank or UNCTAD) calculate their real GDP numbers other than to notice that they’re definitely different-from-each-other-but-qualitatively-similar.

I don’t know of anyone who tries to calculate real GDP at prices from long ago. That would create a difficult operationalization problem: how does one estimate the price of e.g. a smartphone in 1960?

Takeaways

Takeaway 1: Making Predictions Based On Historical Real GDP Growth

I sometimes hear arguments invoke the “god of straight lines”: historical real GDP growth has been incredibly smooth, for a long time, despite multiple huge shifts in technology and society. That’s pretty strong evidence that something is making that line very straight, and we should expect it to continue. In particular, I hear this given as an argument around AI takeoff - i.e. we should expect smooth/continuous progress rather than a sudden jump.

Personally, my inside view says a relatively sudden jump is much more likely, but I did consider this sort of outside-view argument to be a pretty strong piece of evidence in the other direction. Now, I think the smoothness of real GDP growth tells us basically-nothing about the smoothness of AI takeoff. Even after a hypothetical massive jump in AI, real GDP would still look smooth, because it would be calculated based on post-jump prices, and it seems pretty likely that there will be something which isn’t revolutionized by AI. At the very least, paintings by the old masters won’t be produced any more easily (though admittedly their prices could still drop pretty hard if there’s no humans around who want them any more). Whatever things don’t get much cheaper are the things which would dominate real GDP curves after a big AI jump.

More generally, the smoothness of real GDP curves does not actually mean that technology progresses smoothly. It just means that we’re constantly updating the calculations, in hindsight, to focus on whatever goods were not revolutionized. On the other hand, smooth real GDP curves do tell us something interesting: even after correcting for population growth, there’s been slow-but-steady growth in production of the goods which haven’t been revolutionized.

Takeaway 2: Stagnation

On the one hand, growth has been way better than you’d think just from looking at real GDP curves. The internet is indeed pretty awesome, and real GDP basically fails to show it. Same with all the other incredible technology in our lives.

On the other hand… Jason Crawford talks about how a century or two ago, we saw incredibly rapid progress in basically every major industry. Over the past 30 years, we’ve seen incredibly rapid progress in basically one industry: information technology. That, he argues, is the sense in which progress has slowed.

To the extent that real GDP mostly shows growth in the things which aren’t revolutionized, we’d expect it to capture this kind of stagnation pretty well. We’re saying that in the “old days”, basically everything saw rapid progress, so real GDP should have seen rapid growth. Consider housing, for instance: between roughly the 1830’s and the 1960’s we saw the rise of balloon framing, standardization of lumber (e.g. the 2x4), plywood, platform framing, indoor plumbing, etc. This was the era known for bringing the “American dream of homeownership” within reach for most of the working class. It’s not one of the great industrial-era revolutions we hear much about, but economically speaking, housing technology advances were a big deal.

More recently, growth was mostly in information technology, so we should see slower GDP growth. In housing, for instance, the vast majority of new homes still use basically-the-same methods as houses from the second half of the 20th century: concrete foundation, platform frame, plywood, shingles, sheetrock, etc. And indeed, real GDP growth has been noticeably slower over the past 20 years. (Intuitively it seems like growth has been mostly in information technology for ~30-40 years rather than just 20, but with the “chaining” calculation method dramatic one-sector growth does produce pretty good real GDP growth for a few years before prices drop enough that it’s downweighted.)

UPDATE (Oct 14)

Based on the comments, I want to highlight that calculating GDP at e.g. 1960 prices would still not be a good proxy for implied-utility-growth or anything like that, any more than GDP at recent prices is. Price is just generally not a great proxy for value; as maximkazhenkov says in the comments "GDP is more of a measure of economic activity than value". I do think GDP at 1960 prices is basically the right GDP-esque metric to look at to get an idea of "how crazy we should expect the future to look", from the perspective of someone today. After all, GDP at 1960 prices tells us how crazy today looks from the perspective of someone in the 1960's. Also, "GDP (as it's actually calculated) measures production growth in the least-revolutionized goods" still seems like basically the right intuitive model over long times and large changes, and the "takeaways" in the post still seem correct.

Someone should look into Chapter 5 of Capitalism, Socialism and Democracy (Schumpeter) - THE RATE OF INCREASE OF TOTAL OUTPUT. I think there are important insights there